Tech doesn’t always mean software development, backend development or road maps with robotics.

Sometimes, tech is a financial organisation incorporating AI and smart technology systems to drive efficiency and inclusion in the financial sector.

In the past decade, Africa has witnessed a remarkable transformation in its financial landscape, primarily driven by the proliferation of financial technology companies.

This digital revolution has played a pivotal role in addressing the longstanding gender gap in financial inclusion, offering women unprecedented access to financial services, and a seat in the technology world.

Understanding the Existing Gender Gap in Financial Inclusion

Financial inclusion primarily refers to the access to, and use of formal financial services. However, in many African countries, women remain marginalised in this sector.

According to the World Bank’s 2021 Global Findex Database, only 48% women in Sub-Saharan Africa owned financial accounts, compared to 55% of men, indicating a gender gap of 7%.

One of the top factors contributing to this disparity is the prevalence of socio-cultural norms in rural parts of the continent.

According to the 2023 Access to Financial Services in Nigeria (A2F) survey, approximately 28.8 million Nigerians in the northern regions are excluded from the financial system, with women and rural residents being the most affected.

The survey also highlights that the gender gap in financial inclusion widened from 8% in 2020 to 9% in 2023.

This single survey gives us a glimpse into the existing traditional practices that may limit a woman’s right to opening an account, opening a trust fund, owning land, etc. Some restrictions even extend to movement, limiting a woman’s freedom to visit the bank to carry out transactions.

In countries like Cameroon, Nigeria, and Ethiopia, customary laws in certain regions restrict women’s access to land and other financial assets.

For instance, among the Beti people of Southern Cameroon, women cannot inherit land and are only granted food plots by their husbands.

These restrictions on assets could limit a woman’s opportunity to grow her business or invest in her dreams. Assets that she can sell or use to yield money are unavailable to her.

She is left to survive on the meagre amount her husband gives her to cater to the family needs. How, then, does she save enough to do her masters, start a business, or any other thing she has in mind?

Asides societal norms, there is also the issue of the technical requirements that come with traditional banking.

Rural residents in Africa usually cite the absence of necessary identification documents as a barrier to opening accounts. Women with limited education also face difficulties in accessing formal financial systems.

How Fintechs Bridge the Financial Gap in Africa

Fintechs have emerged as a transformative force, offering innovative solutions to bridge the financial inclusion gap in Africa.

Mobile money services, digital lending platforms, and online banking have become accessible alternatives to traditional banking, particularly for underserved populations. Here are some ways fintechs bridge the gender gap in africa:

Easy Access to Credit Services

The woman with no house, no land, or any other financial asset; the woman tossed aside by traditions, restrained from any form of inheritance simply because she is a woman, can now easily access loans and other credit services from fintechs. It doesn’t matter if she is uneducated or unemployed.

It doesn’t matter if she has no land to serve as a collateral; fintechs make it easy for all classes of people in Africa to get loans, invest, own a bank account, and enjoy other financial services.

The technicalities of traditional banking have been erased, as Fintechs leverage alternative data to assess creditworthiness.

Shecluded, a fintech company in Nigeria, focuses on providing financial services to women entrepreneurs, offering loans, savings plans, and financial literacy programs, thus enabling women to access capital for business expansion and personal development.

Kenya’s Tala is another example of a fintech company in Africa that has democratized credit access, empowering women to invest in businesses, education, and healthcare.

Your Bank in Your Pocket

Mobile money services have been at the forefront of fintech innovations in Africa, revolutionizing the way financial transactions are conducted.

These services allow users to store, send, and receive money using their mobile phones, eliminating the need to travel to the bank to make deposits or withdrawals.

As a result, women who are sick, pregnant, uneducated, restricted from moving around, etc., can still access all financial services because they have their banks in their pockets, thanks to fintechs.

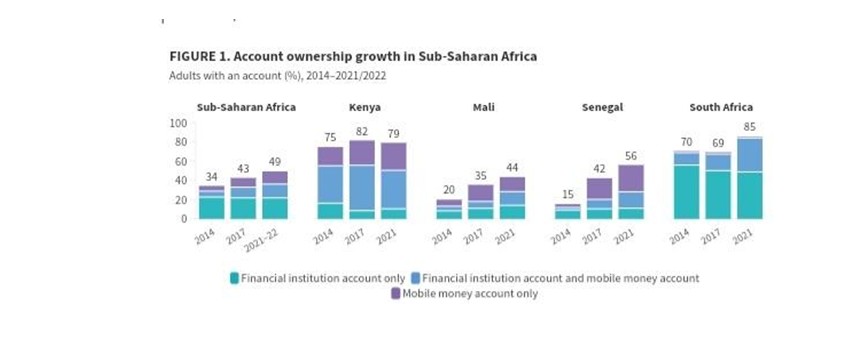

The Global Findex Database 2021: Financial Inclusion, Digital Payments, and Resilience in the Age of COVID-19 indicates that the number of women owning financial accounts in Ghana increased from 54% in 2017 to over 63% in 2021. This increase was primarily driven by the introduction of mobile money accounts.

Other countries in Sub-Saharan Africa have also seen a rapid growth in the number of women and adults who own a bank account, following the introduction of mobile banking.

Driving Savings and Investment Among Women

Driving Savings and Investment Among Women

Fintechs like PiggyVest and ChipperCash encourage users to save by offering flexible savings plans and investment opportunities.

Women benefit from the user-friendly interface and financial management tools of these savings and investment platforms. Fintechs in this category contribute to driving financial literacy across Africa.

The accessibility and convenience encourage many women to manage and grow their finances.

The Effects of Financial Inclusion on Women’s Economic Empowerment

The integration of fintech into Africa’s financial ecosystem has yielded significant benefits for women, some of which include:

- Increased Financial Autonomy: Women now have greater control over their finances, enabling them to make independent decisions, and improving their financial literacy.

- Entrepreneurship Opportunities: Access to credit and savings platforms has empowered women to start and expand businesses. Female entrepreneurs are now more prevalent in Africa. From tailors to store owners and hairdressers, women are empowered to set up their brands, having the assurance of easy loans, deposits and withdrawals. The rise of more entrepreneurs also contributes to economic development and job creation on the continent.

- Improved Household Welfare: With better financial tools, women can invest in health, education, and nutrition, enhancing the overall well-being of their families.

Conclusion

Fintech has proven to be a powerful catalyst in narrowing the gender gap in financial inclusion across Africa, offering women access to essential financial services that were previously out of reach. By this, women in Africa are gaining financial autonomy, building businesses, and improving their household welfare.

Collaborative efforts between governments, fintech companies, and civil society are crucial to sustaining and improving this inclusive financial ecosystem that empower women.

As fintechs continue to reshape Africa’s financial landscape, ensuring that no woman is left behind will not only promote gender equality but also unlock the continent’s full economic potential.